Health insurance claim rejected due to unnecessary treatment India is one of the most frustrating situations for policyholders. You trusted your doctor, followed medical advice, got admitted, and then suddenly the insurer says the treatment was “not required.”

This creates confusion — because from your perspective, the treatment was absolutely necessary. But from the insurer’s side, it may look different.

If you are facing this issue, the important thing to understand is that such rejections are not always final. In many cases, they can be challenged successfully with the right approach.

What Does “Unnecessary Treatment” Mean in Insurance Terms?

When an insurer says a treatment was unnecessary, they usually mean that the hospitalization or procedure was not medically justified based on standard guidelines.

This does not always mean the treatment was wrong — it simply means the insurer believes it could have been avoided or handled differently.

For example:

- Admission for a condition that could be treated with OPD care

- Extended hospital stay without clear reason

- High-cost procedures where simpler alternatives exist

If you want a deeper understanding of how insurers evaluate such cases, it helps to understand how

medical necessity is assessed in health insurance claims in India, as both concepts are closely related.

Why Do Insurers Reject Claims for Unnecessary Treatment?

This decision is usually based on medical review rather than just billing.

Here are the most common reasons:

1. Hospitalization Was Not Required

If the treatment could have been done without admission, the insurer may reject the claim.

2. Lack of Supporting Medical Evidence

If reports or doctor notes do not clearly justify the need for treatment.

3. Short or Routine Procedures

Minor treatments that don’t meet hospitalization criteria.

4. Over-treatment Concerns

Insurers may feel that additional procedures were not essential.

Sometimes, these situations overlap with cases where

hospitalization itself is considered unnecessary by the insurer, leading to similar outcomes.

A Real-Life Scenario Most People Relate To

Let’s take a simple example.

A patient gets admitted for mild chest pain. The hospital advises observation for 24 hours and conducts multiple tests. The bill is submitted for reimbursement.

The insurer reviews the case and says:

“Hospitalization was not medically necessary.”

From the patient’s side, admission felt safer. From the insurer’s side, it may appear excessive.

This difference in perspective is exactly where most claim rejections happen.

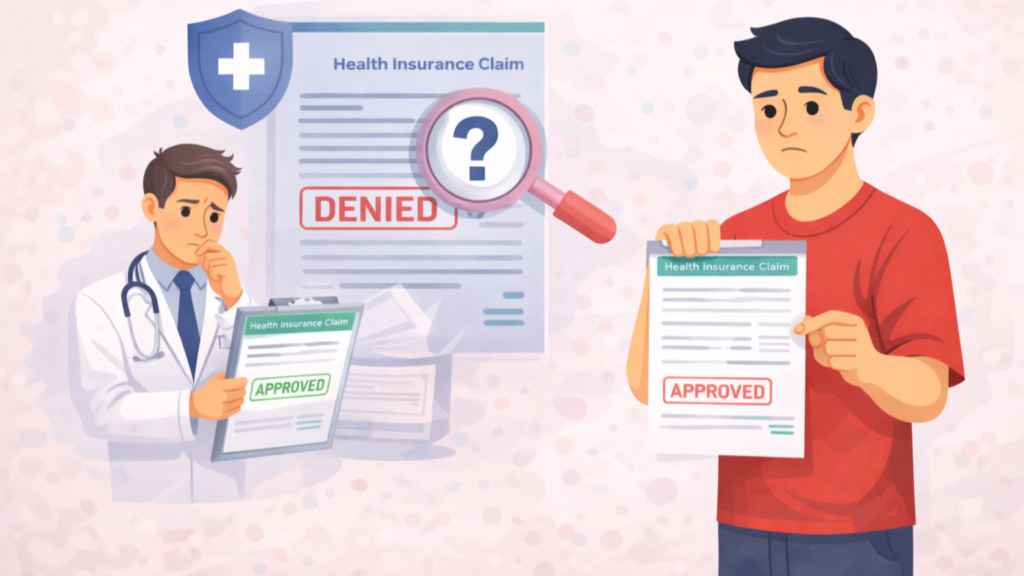

Is This Rejection Always Fair?

Not necessarily.

There are many cases where the insurer does not have complete context. Medical decisions depend on real-time judgment, and sometimes that nuance is missing in documentation.

This is why you should not accept such rejections immediately without reviewing the details.

What You Should Do Immediately After Rejection

Instead of reacting emotionally, follow a structured approach.

Step 1: Read the Rejection Reason Carefully

Understand exactly what the insurer is saying. Look for keywords like “not required” or “not justified.”

Step 2: Review Your Medical Documents

Check if your reports and discharge summary clearly explain the need for treatment.

Step 3: Talk to Your Doctor

This is the most important step. Ask your doctor to provide a written explanation.

A strong medical justification can change the outcome.

Step 4: Submit an Appeal

Once you have proper documents, you can challenge the rejection.

If you’re unsure how to draft your response, this guide on

writing an appeal email for claim rejection in India can help you present your case clearly.

How to Prove Treatment Was Necessary

This is where most appeals succeed or fail.

To strengthen your case, you should provide:

- Doctor’s written justification

- Diagnostic reports showing severity

- Treatment timeline

- Any complications or risk factors

The goal is to show that hospitalization or procedure was not optional — it was required.

Common Mistakes That Lead to Rejection

Many policyholders unknowingly weaken their case due to small mistakes.

- Not keeping complete medical records

- Ignoring discharge summary details

- Submitting unclear or incomplete reports

- Not questioning hospital decisions

Even small gaps in documentation can lead to rejection.

What If the Claim Is Still Not Approved?

If your appeal does not work, don’t assume there are no options left.

You can escalate the issue further through the insurer’s grievance system.

If required, you can also approach the Insurance Regulatory and Development Authority of India (IRDAI) for resolution.

Understanding the complete escalation path helps, and this explanation of

how to appeal insurance claim denial in India can guide you through the next steps.

A Practical Tip That Can Change the Outcome

Always ensure that your discharge summary clearly mentions the reason for hospitalization.

This single document plays a major role in claim decisions.

If needed, request the hospital to update it with more detailed clinical justification.

When Insurer May Be Right

It’s also important to be realistic.

There are cases where the insurer’s decision may actually be valid.

- Hospital admission for minor conditions

- Unnecessary diagnostic tests

- Luxury or precautionary hospitalization

Understanding this helps you decide whether to appeal or accept the decision.

How Insurers Decide Whether a Treatment Was Necessary

Many policyholders assume that claim decisions are made only based on bills and documents. In reality, insurers often involve medical experts to review the case.

These experts evaluate whether the treatment followed standard medical practices and whether hospitalization was justified.

They usually check:

- The severity of symptoms at the time of admission

- Diagnostic test results

- Treatment provided during hospitalization

- Duration of hospital stay

If these factors do not strongly support the need for admission or procedure, the claim may be marked as unnecessary treatment.

This is why even genuine cases sometimes get rejected — not because treatment was wrong, but because it was not clearly documented.

Difference Between Doctor’s Advice and Insurance Approval

This is one of the most misunderstood areas.

Patients usually trust their doctor’s advice completely, which is the right thing to do from a medical perspective. However, insurance approval works differently.

A doctor focuses on patient safety and may recommend admission as a precaution. But insurers look at whether that admission was essential based on policy terms.

This difference in approach leads to many claim disputes.

Understanding this gap helps you prepare better documentation rather than assuming the insurer is always wrong.

How to Strengthen Your Case Before Submitting a Claim

If you are still in the treatment stage or planning a claim, a few proactive steps can make a big difference.

- Ask the doctor to clearly mention the reason for admission

- Ensure all symptoms and observations are documented

- Keep copies of test reports and prescriptions

- Inform the insurer or TPA on time

These small actions can prevent rejection due to unclear justification.

Situations Where Rejection Can Be Reversed Successfully

Not all unnecessary treatment rejections are final.

Many cases get approved after proper clarification, especially when:

- Additional medical evidence is submitted

- Doctor provides a detailed justification

- Initial documents were incomplete

- Insurer misunderstood the treatment context

This is why it’s important to treat rejection as a step in the process, not the final outcome.

When You Should Consider Escalation Seriously

If you have submitted all valid documents and still receive no proper response, escalation becomes necessary.

You should consider this step when:

- Your claim is rejected without clear reasoning

- The insurer does not respond within expected timelines

- You strongly believe your case is medically justified

At this stage, raising a formal complaint can help move your case forward.

Final Thoughts

Facing a health insurance claim rejected due to unnecessary treatment India situation can feel unfair, especially when you followed medical advice.

But these cases often come down to documentation and justification.

If you can clearly demonstrate that the treatment was necessary, there is a strong chance of getting your claim reconsidered.

The key is to act quickly, stay informed, and approach the situation logically rather than emotionally.